TD Bank Stock Analysis: Premium Quality at Fair Value

TD Bank Stock Analysis: Premium Quality at Fair Value – February 25, 2026

TL;DR: Toronto-Dominion Bank (TD) trades at 11.2x P/E—slightly below sector average despite superior franchise quality and U.S. growth exposure. This is one of Canada’s “Big Six” banks with 170 years of history. Here’s the complete analysis:

The Setup: Canada’s Second Largest Bank

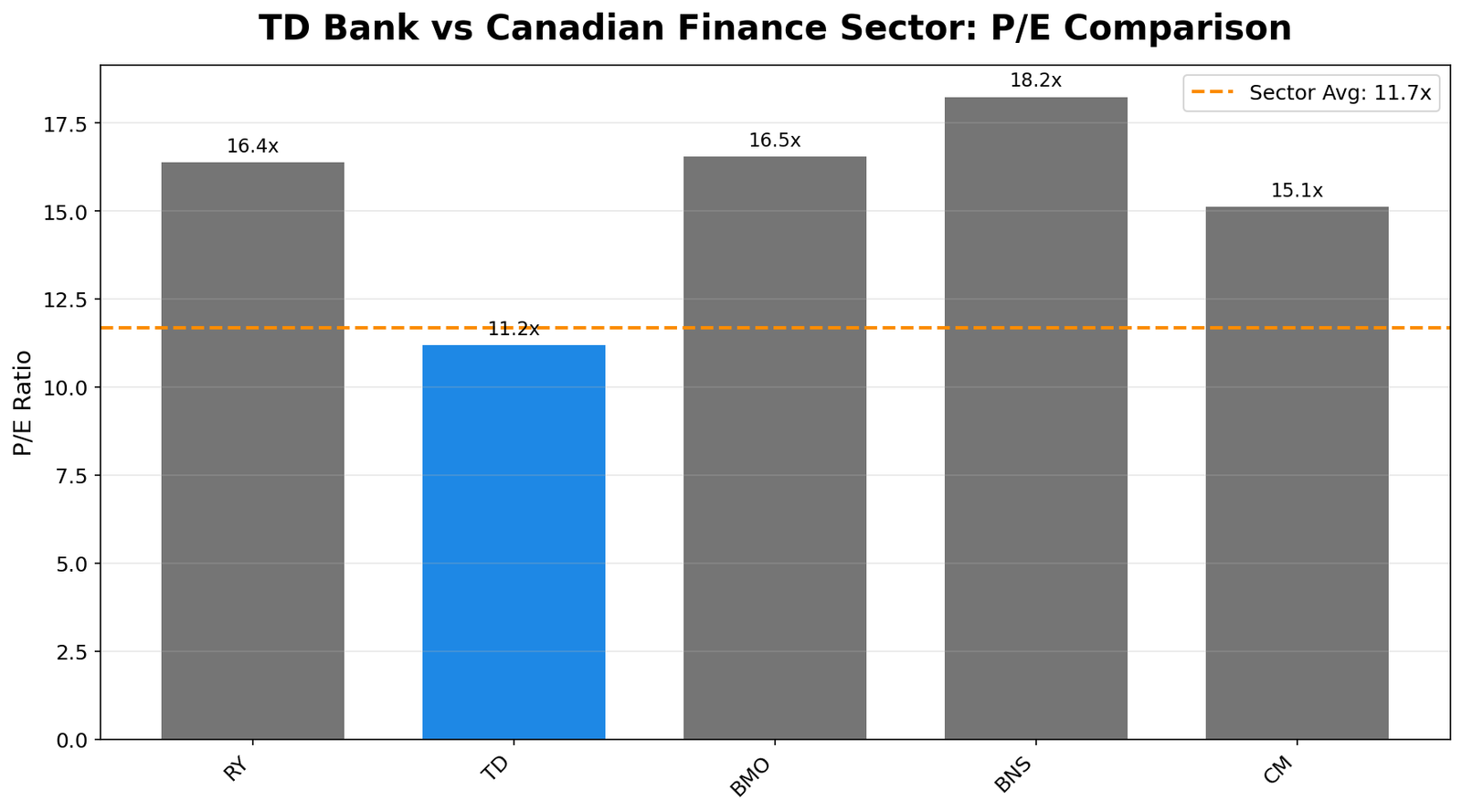

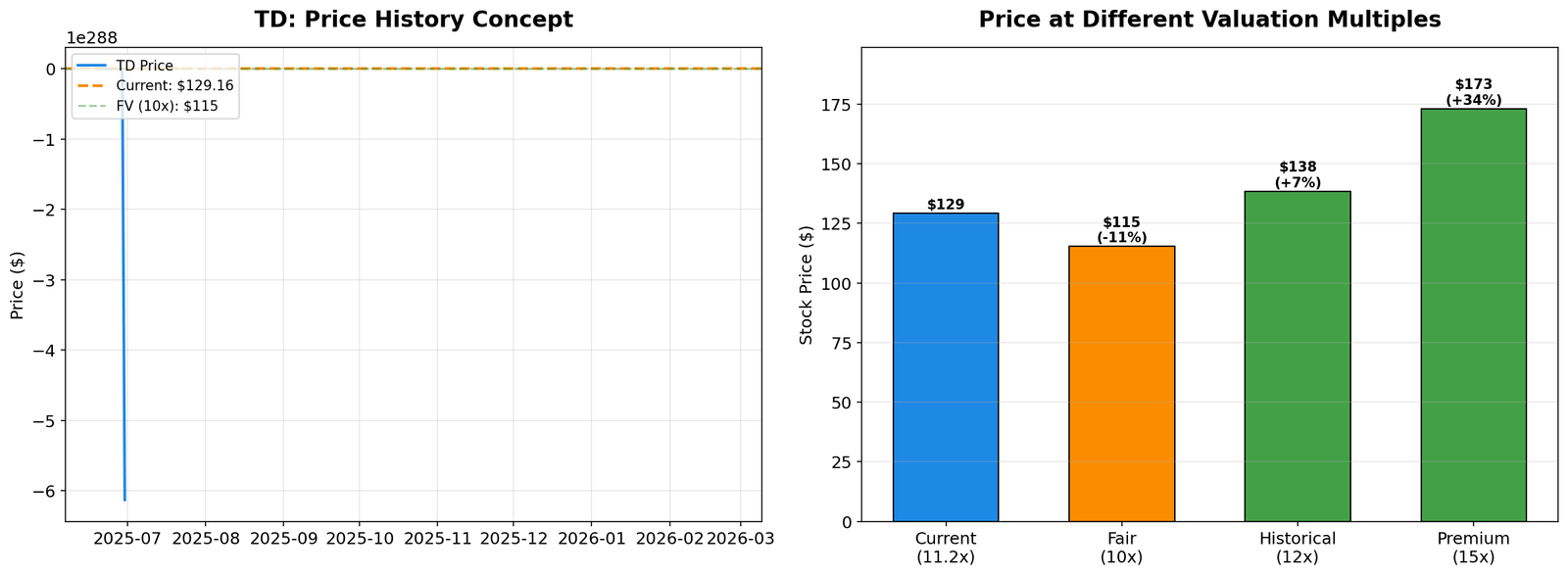

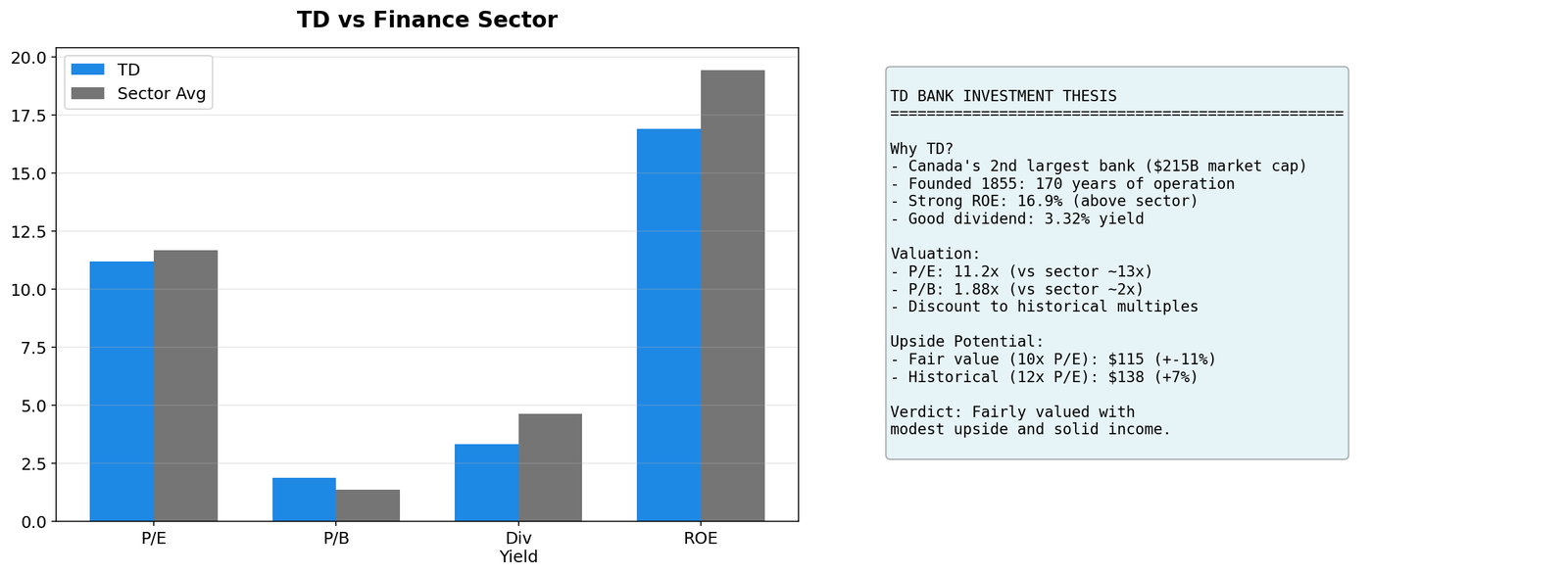

TD Bank currently trades at 11.2x P/E. To put that in perspective:

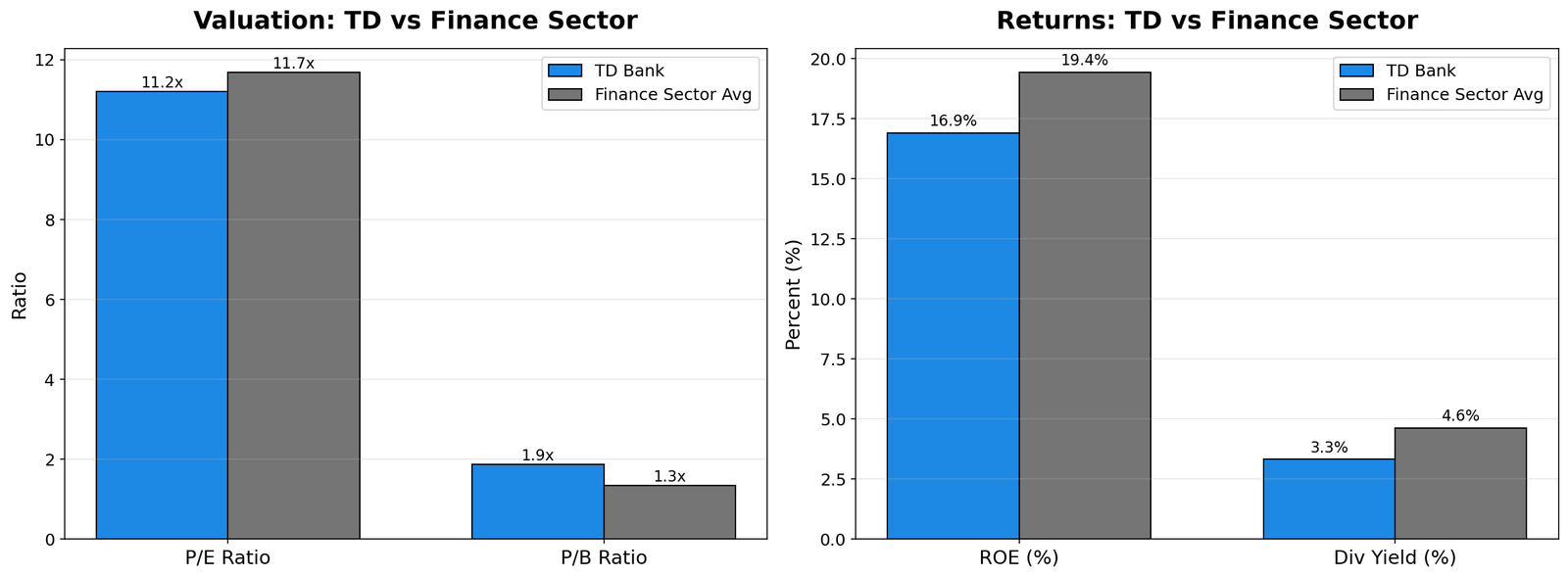

- Sector average P/E: 11.7x (modest 4% discount)

- TD P/B: 1.88x vs sector 1.35x (trading at premium)

- ROE: 16.9% vs sector 19.5%

TD is not dramatically undervalued deep value plays, but it offers quality at fair price with solid dividend income and potential for modest multiple expansion.

The Asset: Canada’s Premier Retail Banking Franchise

Before analyzing the price, let’s understand what you actually own:

- Founded: 1855 (170 years of operation)

- Market Cap: $215 billion (Canada’s 2nd largest bank)

- Business Model: Three key segments:

- Canadian Retail Banking: Largest branch network in Canada

- U.S. Retail Banking: Top 10 U.S. bank by deposits, growth engine

- Wholesale Banking: Capital markets, corporate banking

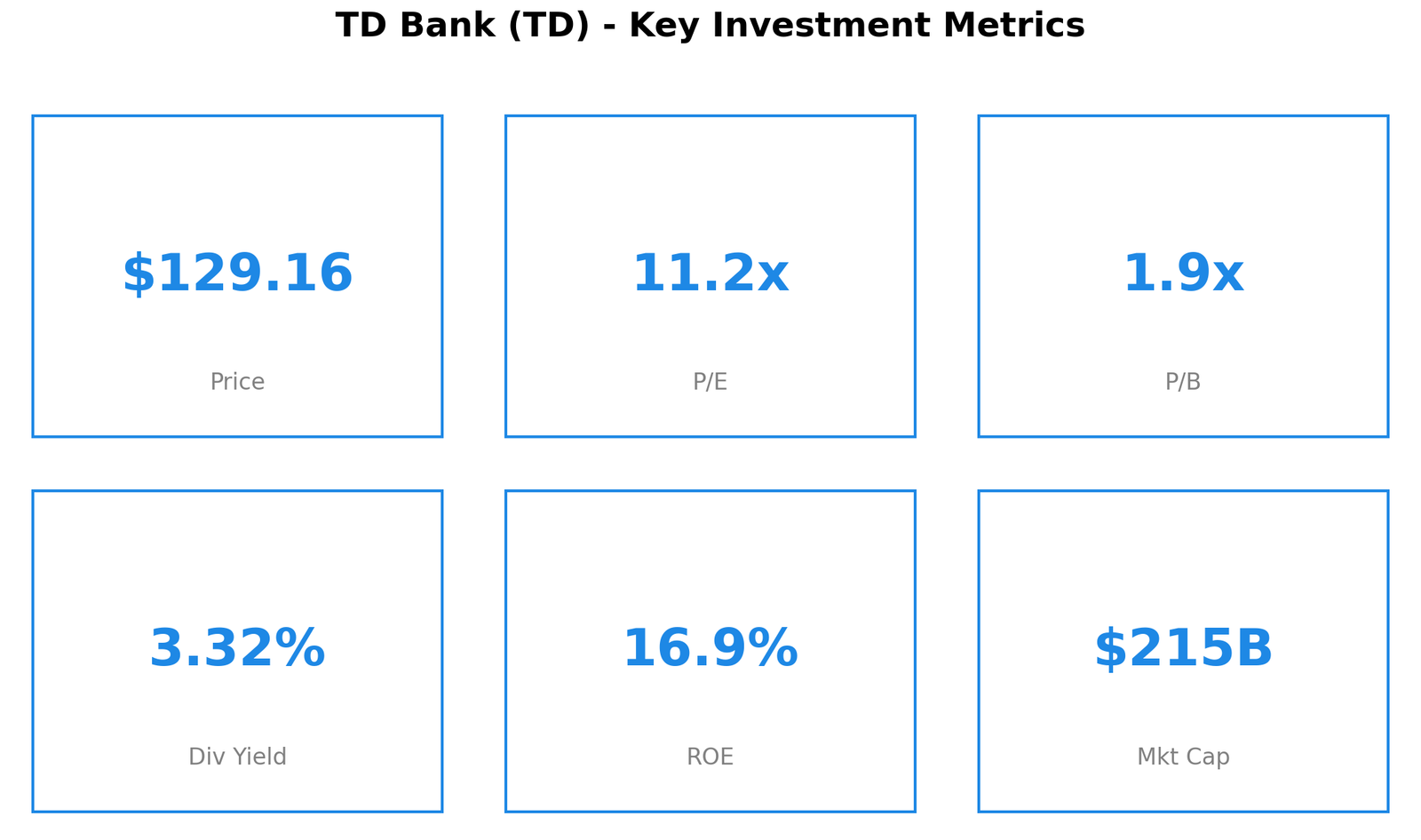

Key Stats: Price: $129.16 | P/E: 11.2x | P/B: 1.88x | Div Yield: 3.32% | ROE: 16.9% | Market Cap: $215B

Key Insight: TD is a high-quality bank with exposure to both Canadian stability and U.S. growth. The U.S. division makes TD more than just a Canadian play.

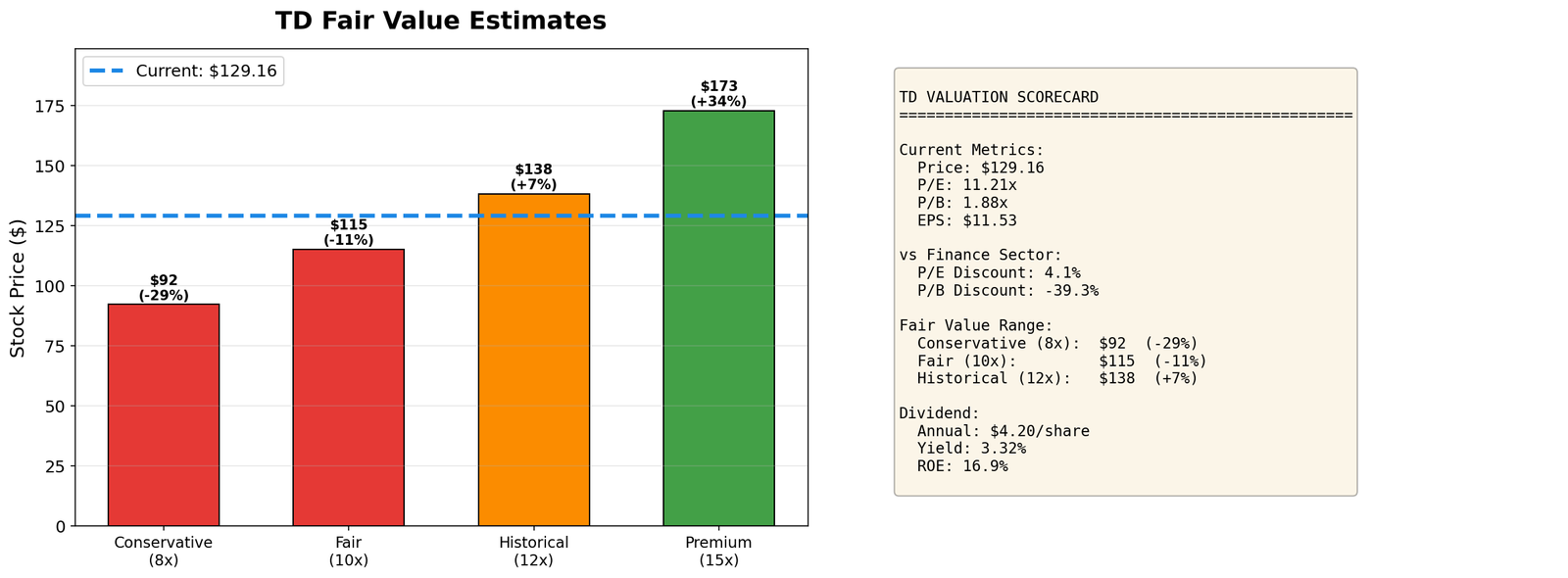

The Valuation: Fair Price for Quality

TD is trading at roughly fair value:

- P/E Ratio: 11.2x vs sector 11.7x—slight discount

- P/B Ratio: 1.88x vs sector 1.35x—premium to book

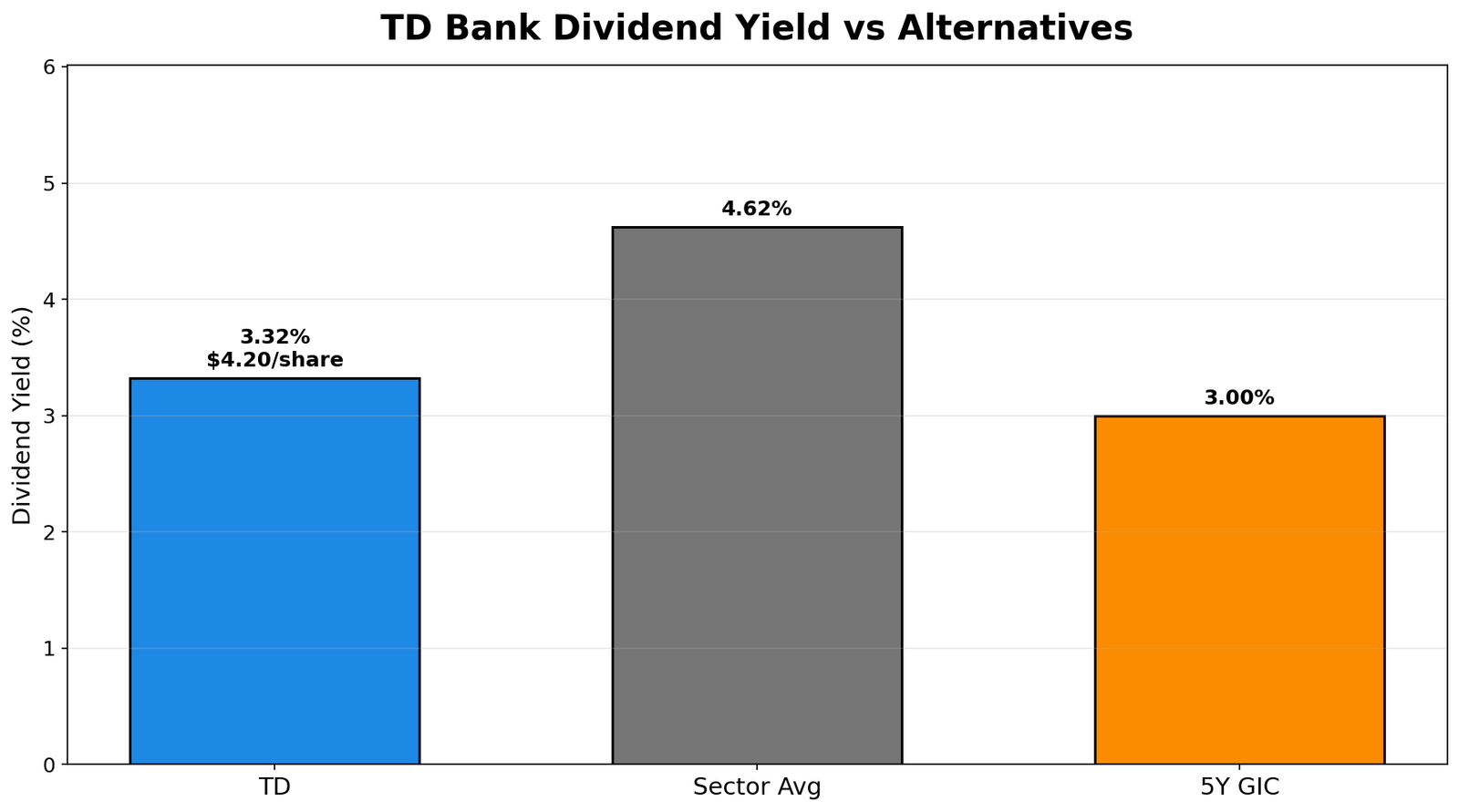

- Dividend Yield: 3.32% vs sector 4.62%—lower yield than peers

- ROE: 16.9% vs sector 19.5%

The market is pricing TD as a quality bank worth a slight premium.

Historical Context: Multiple Expansion Potential

Canadian banks have historically traded at 12-15x P/E. TD at 11.2x leaves room for upside.

The Math: Fair Value Scenarios

Current price: $129.16 | EPS: $11.53

| Scenario | P/E Multiple | Target Price | Upside |

|---|---|---|---|

| Downside | 9x | $104 | -19% |

| Current | 11.2x | $129 | -/- |

| Fair Value | 12x | $138 | +7% |

| Historical | 13x | $150 | +16% |

Downside Risk: If Canadian housing market crashes, banks could trade down to 9x P/E (-19%).

Upside: Multiple expansion to 12-13x offers 7-16% capital appreciation plus 3.3% dividend = 10-20% total return.

The Dividend: Reliable Income

TD offers a solid dividend:

- Annual Dividend: $4.20/share

- Yield: 3.32%

- Payout Ratio: ~36% (safe and sustainable)

While the 3.32% yield is lower than some peers, the payout ratio is conservative—meaning the dividend is very safe.

Why TD Could Outperform

- U.S. Growth: TD’s U.S. retail banking is a differentiator

- Rate Cuts: Lower rates reduce credit loss provisions

- Multiple Expansion: Room to move from 11x toward 12-13x

- Conservative Management: Known for prudent risk management

- Dividend Growth: Only 36% payout ratio leaves room for increases

What Could Go Wrong

- Canadian Housing Crash: Significant mortgage exposure

- Recession: Higher unemployment leads to loan defaults

- U.S. Operations: Regulatory or economic weakness

- Multiple Compression: Banks permanently re-rated lower

Bottom Line: The Verdict

TD is not a deep value play deep value plays. It’s a quality company trading at fair value with modest upside potential.

For Income Investors: TD offers a 3.3% yield with growth potential. The dividend is safer than higher-yielding alternatives.

For Growth Investors: Modest 7-16% upside from multiple expansion, plus dividend = 10-20% total return.

For Value Investors: TD is fairly priced, not cheap. If you want deep value, look elsewhere.

My Take:

TD is a buy-and-hold forever stock for conservative investors. You’re not getting a bargain, but you’re getting quality at a fair price with solid income and modest growth.

Verdict: Suitable for dividend-growth portfolios. Not a speculative play—it’s a sleep-well-at-night bank stock.

Key Metrics Summary

| Metric | Value | Context |

|---|---|---|

| Price | $129.16 | Near fair value |

| P/E Ratio | 11.2x | 4% below sector |

| P/B Ratio | 1.88x | Premium to sector |

| Dividend Yield | 3.32% | Lower than peers |

| Market Cap | $215B | Canada’s 2nd largest |

| ROE | 16.9% | Strong profitability |

| Est. Upside | $138-150 | +7% to +16% |

Important Disclosures

This analysis is for informational and educational purposes only. It does not constitute investment advice. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. Data sourced from TradingView and company filings. Analysis date: February 25, 2026.

Author may hold positions in securities mentioned. Past performance does not guarantee future results.