Constellation Software (CSU) Analysis: Premium Growth at a Precarious Price

Constellation Software Stock Analysis: Premium Growth or Overvalued? – February 26, 2026

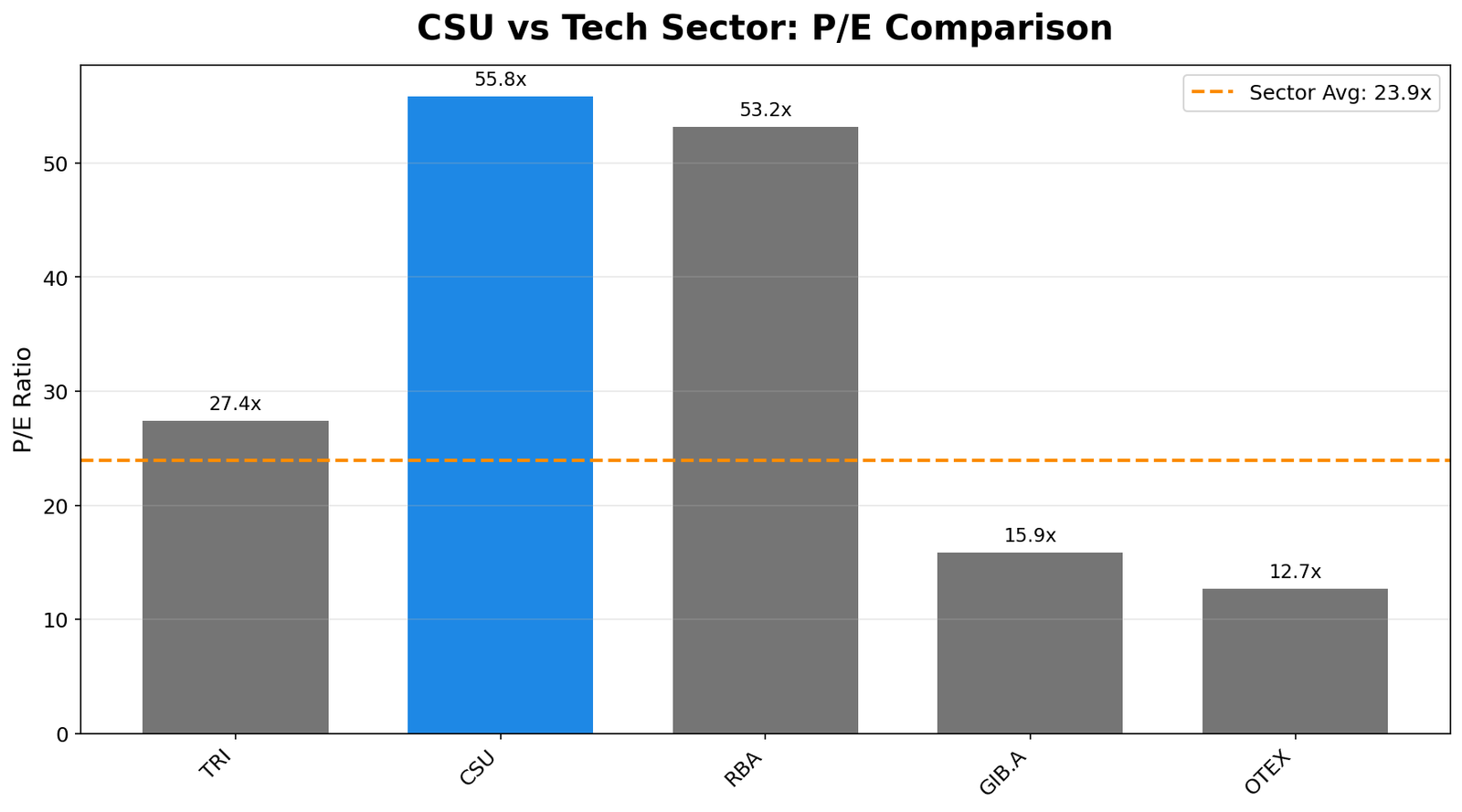

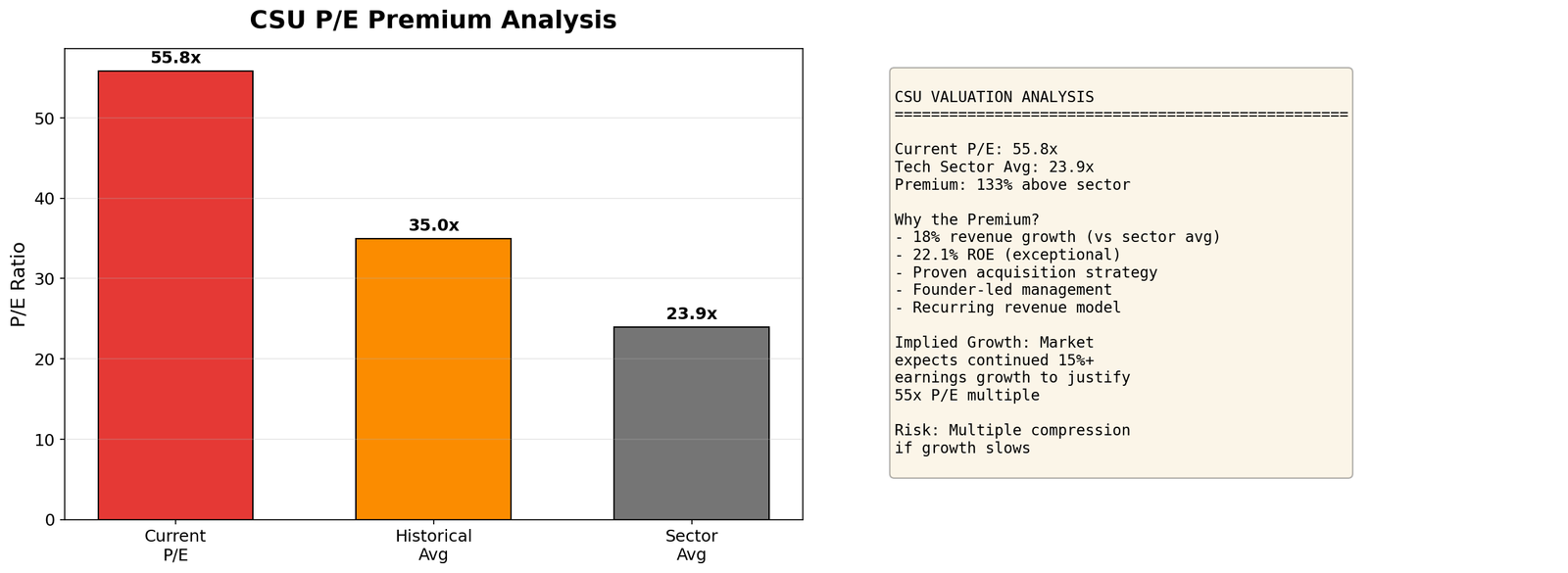

TL;DR: Constellation Software (CSU) trades at 55.8x P/E, nearly 2.5x the tech sector average. Revenue growing 18% with 22% ROE. This is a compounder that’s priced for perfection. Here’s the full analysis.

The Setup: The Canadian Software Compounder

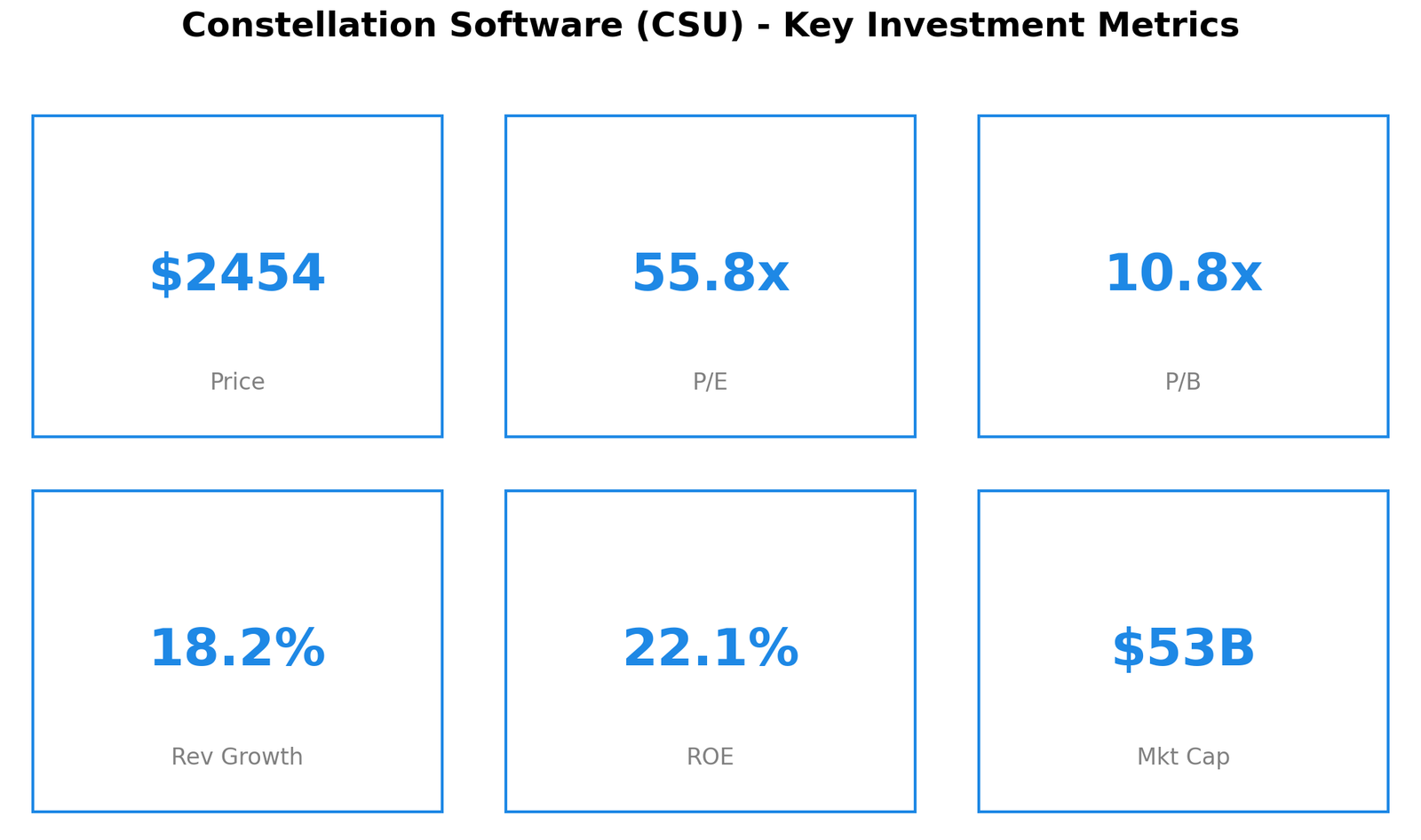

Constellation Software (TSX: CSU) currently trades at $2,454 per share with a 55.8x P/E. To put that in perspective:

- Tech sector average P/E: 23.9x

- CSU P/E: 55.8x (133% premium)

- Current market cap: $53.3 billion

The core question: Is 18% revenue growth worth paying 2.5x the sector multiple?

The Asset: The Acquisition Machine

Before analyzing the price, let’s understand what you actually own:

- Founded: 1995 by Mark Leonard (30 years in operation)

- Market Cap: $53.3 billion

- Business Model: Acquires smaller vertical market software (VMS) companies

- Over 150 acquisitions since inception

- Focuses on niche software markets

- Decentralized operating model

- Recurring revenue base

- Key Stats:

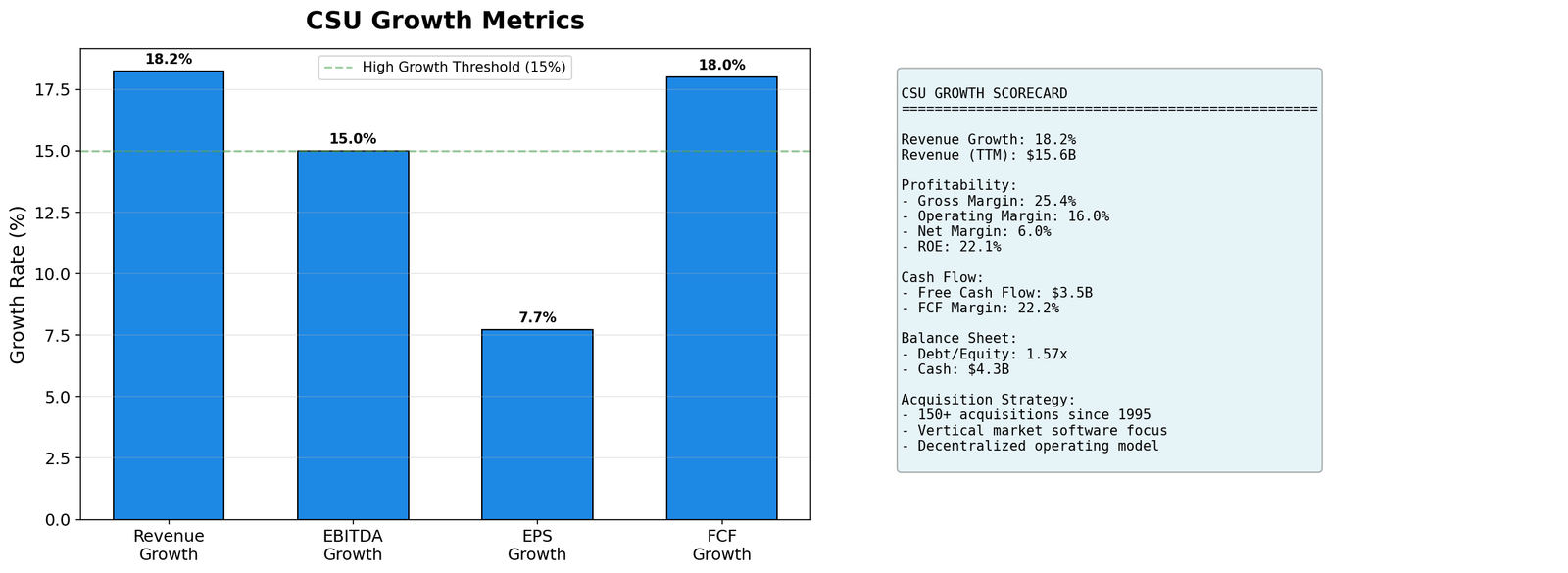

- Revenue: $15.6 billion (TTM)

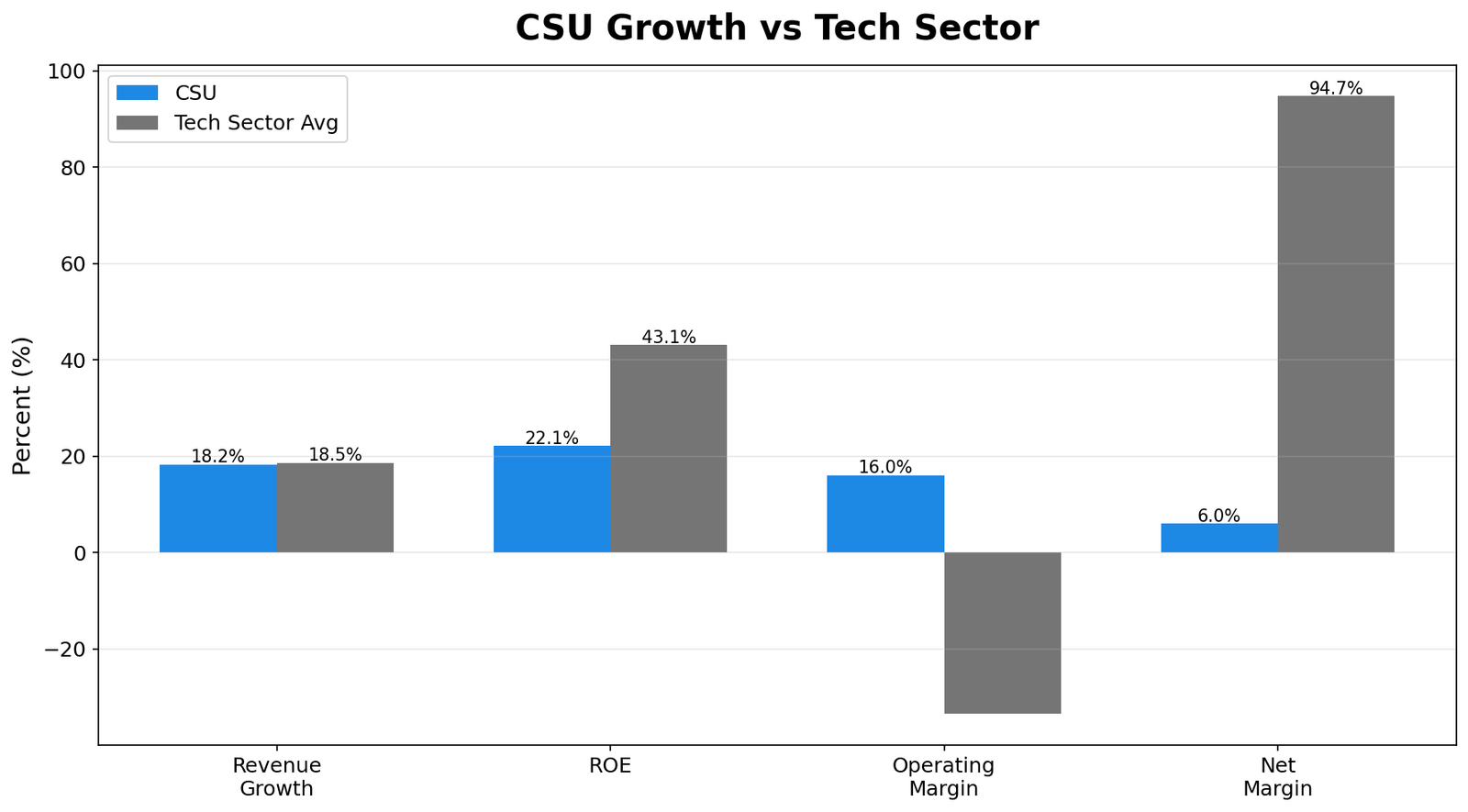

- Revenue growth: 18.2%

- EPS: $43.96

- ROE: 22.1%

- P/B: 10.78x

- Dividend yield: 0.23% (minimal)

The Valuation: Priced for Perfection

At 55.8x P/E, CSU is trading at a massive premium:

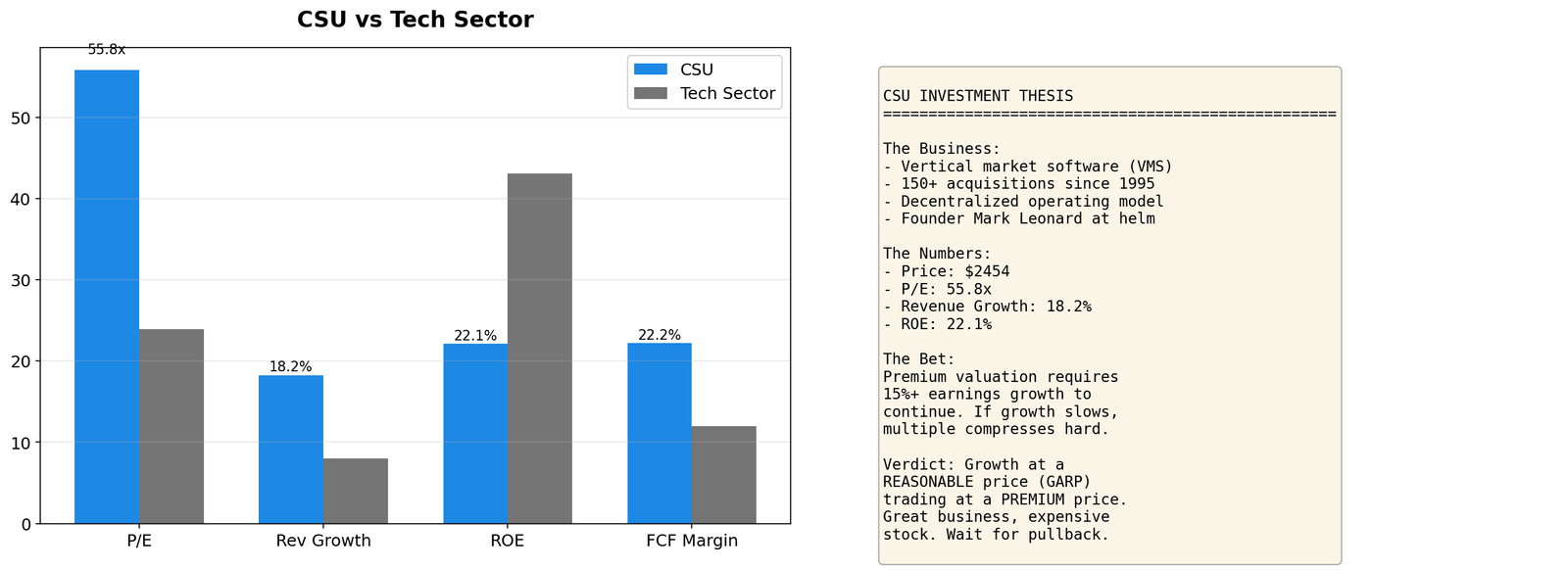

- P/E Ratio: 55.8x vs sector 23.9x (133% premium)

- P/B Ratio: 10.78x vs sector 5.57x (94% premium)

- ROE: 22.1% vs sector 43.1% (lower than average)

- Revenue Growth: 18.2% vs sector 8% (2.3x faster growth)

The premium is justified by growth, but 55x P/E leaves almost no room for disappointment.

Historical Context: The Compound Returns

CSU has been one of Canada’s best-performing stocks over the past decade:

- 10-year return: Over 1,300%

- Stock has split multiple times

- Multiple expansion drove much of the gains

- Original shareholders have life-changing returns

The challenge: Past returns don’t guarantee future results.

The Math: Growth Required to Justify Price

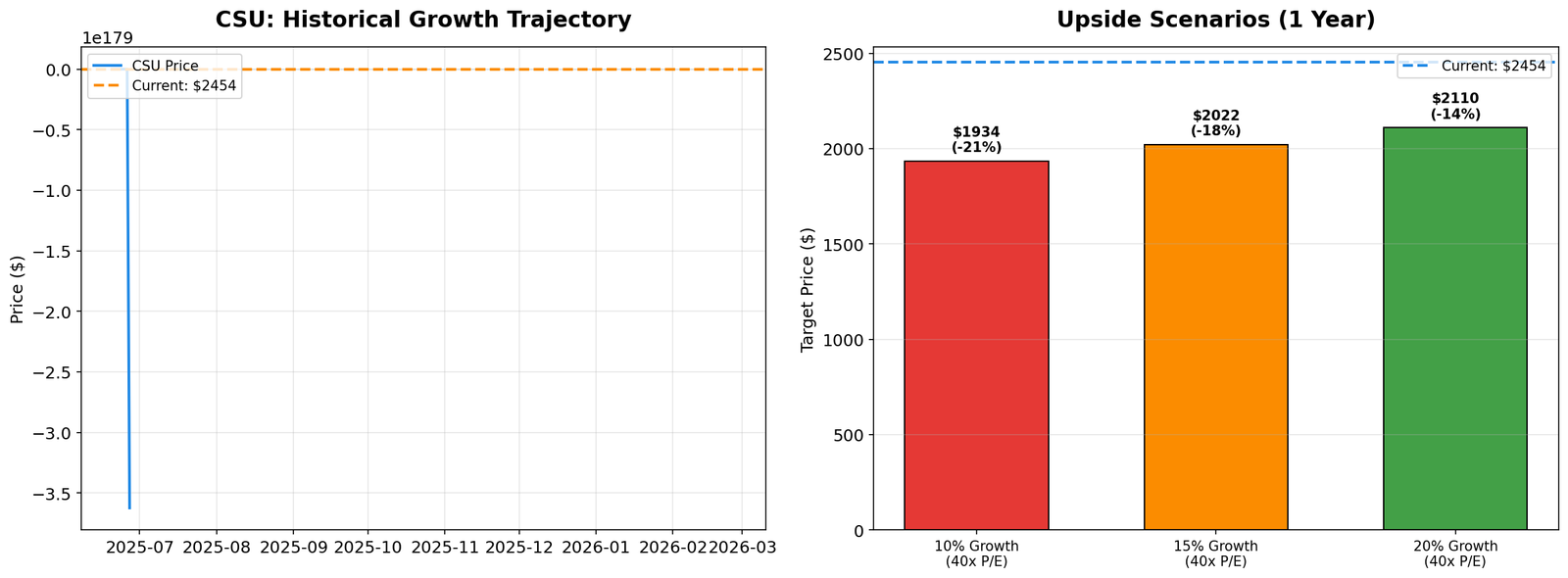

Current EPS: $43.96 | Price: $2,454

| Growth Rate | Future EPS | At 40x P/E | Upside |

|---|---|---|---|

| 10% | $48.36 | $1,934 | -21% |

| 15% | $50.56 | $2,022 | -18% |

| 20% | $52.75 | $2,110 | -14% |

| 25% | $54.95 | $2,198 | -10% |

The Reality: Even with 25% EPS growth, multiple compression to 40x P/E would result in -10% downside. The stock is priced for sustained 30%+ EPS growth combined with a maintained 55x multiple.

Why It Could Work (Bull Case)

- Acquisition Pipeline: Thousands of potential VMS acquisition targets exist. CSU’s playbook is proven.

- Recurring Revenue: Vertical market software customers rarely switch. Stickiness creates predictable cash flows.

- Decentralized Model: Minimal central overhead. Acquired companies keep autonomy. Better than typical conglomerate approach.

- Mark Leonard: Founder-CEO with 30 years of execution. Still actively involved. Proven capital allocator.

- Growth Runway: International expansion just beginning. European markets underpenetrated.

What Could Go Wrong (Bear Case)

- Acquisition Exhaustion: Good deals become scarce. Competition for VMS companies increases. Prices paid escalate.

- Multiple Compression: Any growth disappointment triggers massive P/E contraction. 55x multiple has 50% downside to 25-30x.

- Size Challenge: At $53B market cap, smaller acquisitions barely move needle. Need $5B+ deals for material impact.

- Management Transition: Mark Leonard won’t run company forever. Culture could change.

- Macro Risk: Recession crushes growth stock multiples regardless of business quality.

Bottom Line: The Verdict

CSU is a great business trading at a dangerous price.

For Growth Investors: The 18% revenue growth is attractive, but 55x P/E requires perfection. Better opportunities likely exist elsewhere.

For Value Investors: Stay away. This is the opposite of value investing. Paying 133% premium to sector for growth already priced in.

For Momentum Investors: The trend is your friend until it isn’t. Works until growth slows.

My Take:

CSU is a compounder priced as a hypergrowth stock. The business is high quality, but the valuation assumes flawless execution forever. At 55x P/E, one earnings miss could trigger 30-40% decline.

Verdict: Wait for a better entry. Worth buying at 30-35x P/E (~$1,300-1,500) after a correction. Until then, the asymmetric risk/reward favors patience.

Key Metrics Summary

| Metric | Value | Context |

|---|---|---|

| Price | $2,454 | High multiple |

| P/E Ratio | 55.8x | 133% above sector |

| Market Cap | $53.3B | Large cap |

| Revenue Growth | 18.2% | Strong growth |

| ROE | 22.1% | Quality returns |

| Est. Fair Value | $1,300-1,500 | 30-35x P/E |

Important Disclosures

This analysis is for informational and educational purposes only. Data sourced from TradingView. Analysis date: February 26, 2026.