NorthWest Healthcare REIT (NWH.UN) Analysis: Deep Value or Value Trap?

NorthWest Healthcare REIT Stock Analysis: Trading Below Book Value – February 27, 2026

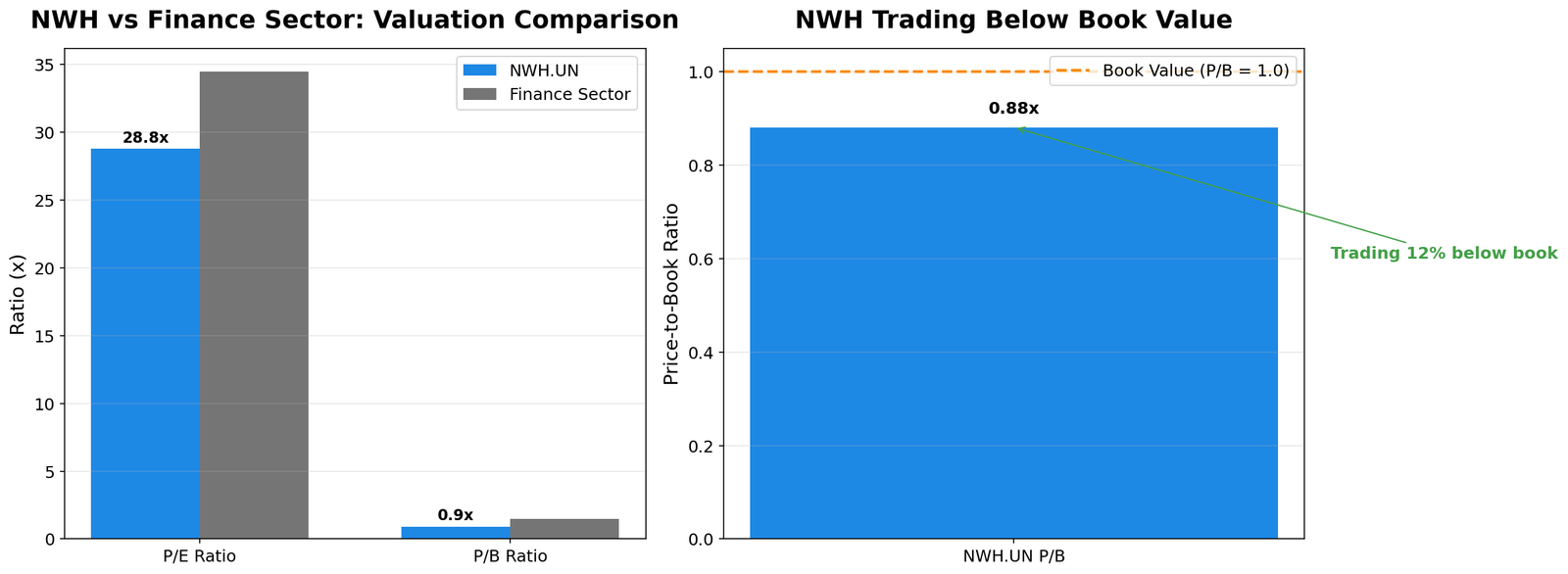

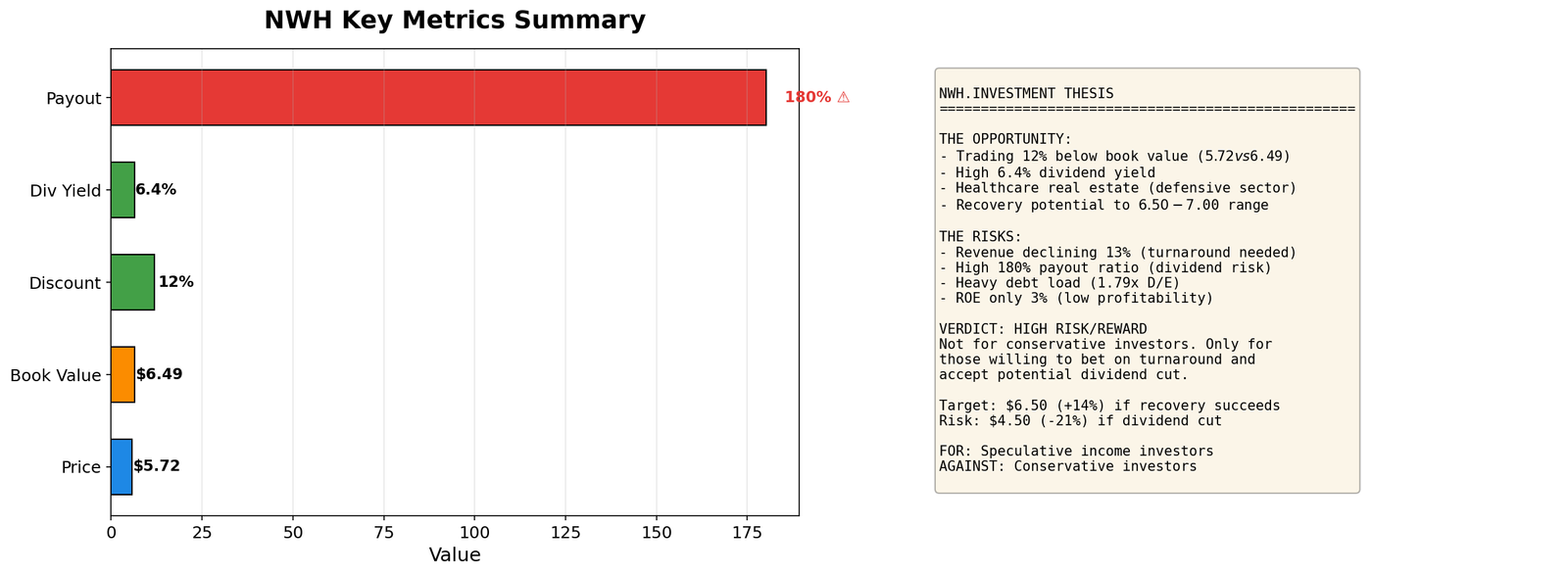

TL;DR: NorthWest Healthcare REIT (NWH.UN) trades at $5.72, 12% below book value, with a 6.4% dividend yield. But revenue is declining 13%, payout ratio is 180%, and debt is high at 1.79x equity. This is either a deep value opportunity or a value trap. Here’s the full analysis.

The Setup: Trading Below Book Value

NWH.UN currently trades at $5.72 per share with a price-to-book ratio of just 0.88x. This means:

- Book value per share: $6.49

- Current price: $5.72

- Trading 12% below book value

- Market cap: $1.4 billion

The core question: Is this a bargain basement healthcare REIT, or a classic value trap?

The Asset: Healthcare Real Estate

Before analyzing the price, let’s understand what you actually own:

- Asset Class: Healthcare real estate investment trust (REIT)

- Hospitals, medical offices, clinics

- International portfolio (Canada, Europe, Australasia)

- Defensive sector (healthcare)

- Market Cap: $1.4 billion

- Key Stats:

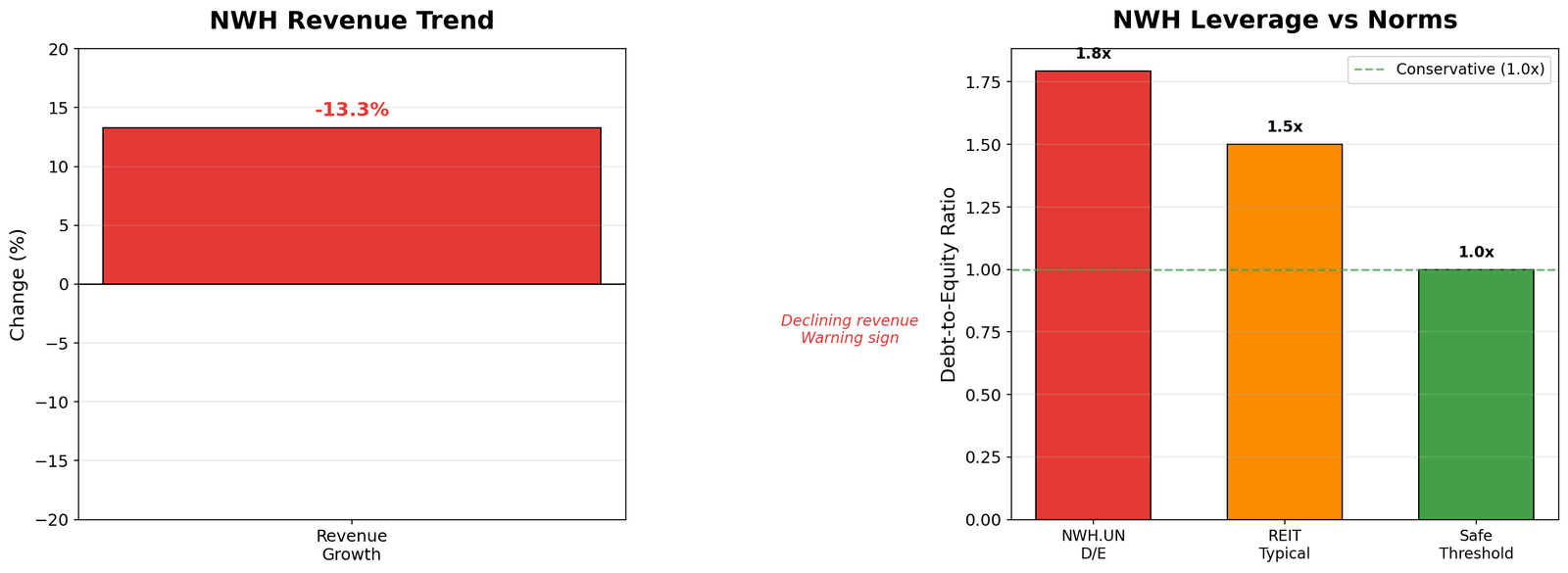

- Total Revenue: $433M (TTM)

- Revenue growth: -13.3% (declining)

- Gross margin: 74.4%

- Operating margin: 55.9%

- P/E: 28.8x

- P/B: 0.88x (below book)

- Dividend yield: 6.44%

The Valuation: Below Book But Risky

At 0.88x P/B, NWH is trading below book value:

- P/B Ratio: 0.88x (40% below sector average of 1.46x)

- Dividend Yield: 6.44% vs sector 4.45% (45% premium)

- Revenue Growth: -13.3% (red flag)

- ROE: 3.04% (very low)

The discount exists because the market is pricing in risk. Trading below book is rare for REITs and usually signals trouble.

The Red Flags: Why It’s Cheap

NWH trades below book for reasons:

- Declining Revenue: -13% year-over-year

- Low Profitability: ROE of 3% is terrible for a REIT

- High Leverage: Debt-to-equity of 1.79x is aggressive

- Dividend Risk: Payout ratio of 180% (not covered by earnings)

- 5-Year Performance: -57% (massive destruction of value)

This isn’t a hidden gem. The market knows something is wrong.

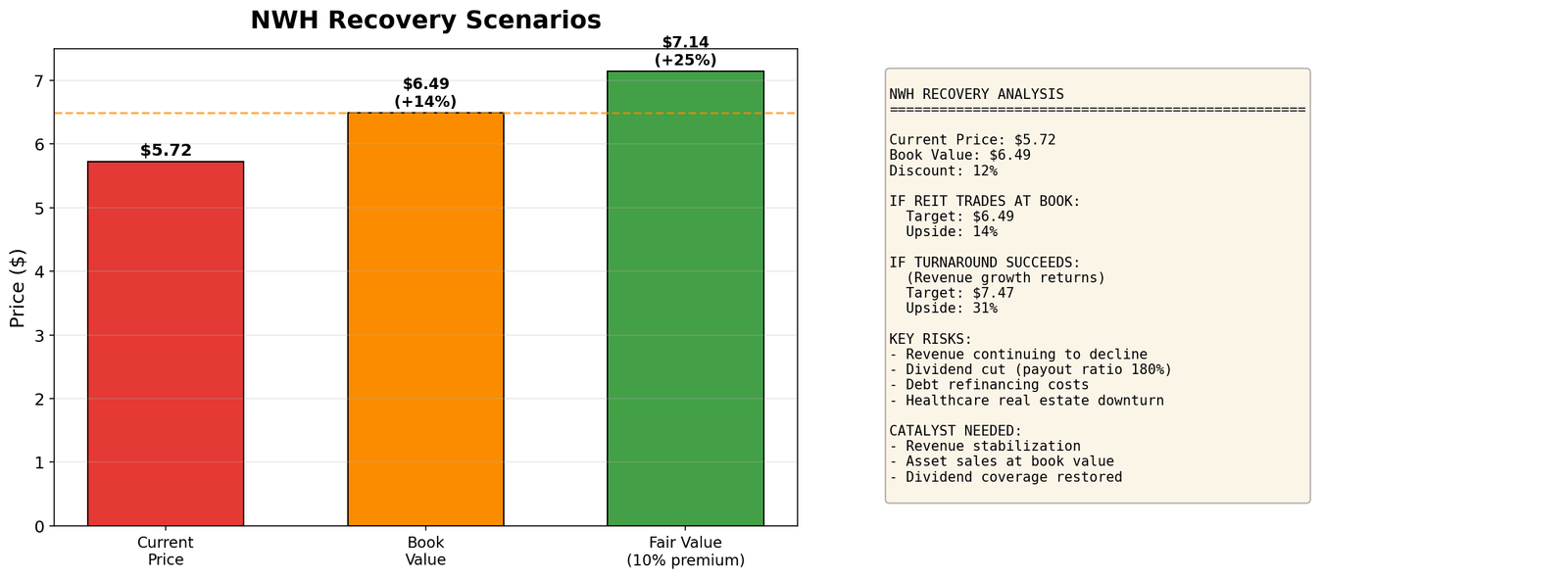

The Math: Recovery Scenarios

Current price: $5.72 | Book value: $6.49

| Scenario | Target Price | Upside |

|---|---|---|

| Trade to Book Value | $6.49 | +13% |

| Fair Value (10% premium) | $7.14 | +25% |

| Turnaround Success | $8.00 | +40% |

| Dividend Cut (bear case) | $4.50 | -21% |

The Reality: Even reaching book value requires confidence to return. That’s a big if.

Why It Could Work (Bull Case)

- Below Book Value: Asset values support the price

- High Yield: 6.4% dividend while you wait

- Defensive Sector: Healthcare real estate tends to be stable

- Turnaround Potential: New management could improve operations

- Recent Strength: +12% YTD vs -57% over 5 years (momentum shift?)

What Could Go Wrong (Bear Case)

- Dividend Cut: 180% payout ratio is unsustainable

- Continued Decline: Revenue keeps dropping

- Debt Pressure: High leverage becomes a burden in high rate environment

- Asset Write-Downs: Book value might be overstated

- Value Trap: Cheap for a reason – could get cheaper

Bottom Line: The Verdict

NWH is a speculative turnaround bet, not an investment.

For Income Investors: The 6.4% yield is tempting but risky. A dividend cut would crush the stock. Better REITs exist.

For Value Investors: Trading below book is interesting, but only if assets are worth book. Needs deep due diligence.

For Growth Investors: This is the opposite of what you want. Declining revenue, low ROE.

My Take:

NWH is a high-risk, potentially high-reward speculation. The discount to book and high yield create a tempting entry, but the declining revenue and unsustainable payout ratio are serious red flags. This is only for investors willing to bet on a turnaround and accept potential capital loss.

Verdict: Pass for most investors. If you must speculate, keep position small (under 2% of portfolio), use limit orders below $5.50, and set a stop loss at $4.75. This is not a core holding.

Key Metrics Summary

| Metric | Value | Context |

|---|---|---|

| Price | $5.72 | Below book |

| P/B Ratio | 0.88x | 40% below sector |

| Dividend Yield | 6.44% | High but risky |

| Revenue Growth | -13.3% | Declining (red flag) |

| Payout Ratio | 180% | Not sustainable |

| Debt/Equity | 1.79x | High leverage |

| 5-Year Return | -57% | Massive underperformance |

Important Disclosures

This analysis is for informational and educational purposes only. It does not constitute investment advice. Always conduct your own research and consult with a qualified financial advisor before making investment decisions. Data sourced from TradingView. Analysis date: February 27, 2026.

Author does not hold positions in securities mentioned. Past performance does not guarantee future results. Investing in REITs involves risks including potential for significant capital loss.